57 / 98

57 / 98

57

4

Administration

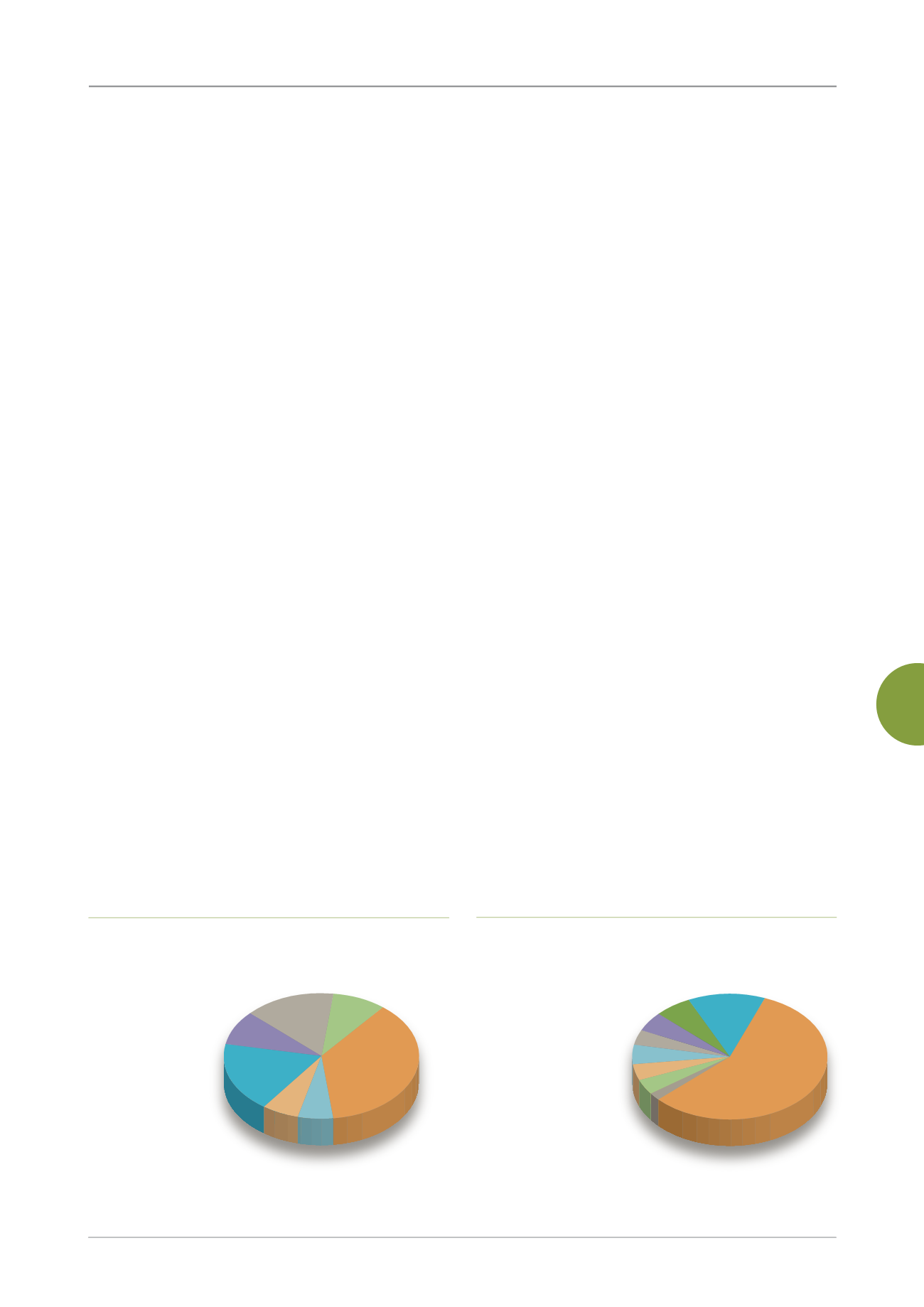

Figure 11 Audits (2014)

Accounting and

Cash Operations 18%

Services

Management 9% ..............

Planning and

Management 15% .................................

..............

Property and Assets 6% .....................................

57% Operations

13% Personnel

.....................

........................................

.......................................

........

6% Payroll Affairs

9% Lending

and Investment

37% Operations

...........................

...........................

........................................

...........................................

.......................................

.............................

Figure 12 Audit Suggestions (2014)

Accounting and

Cash Operations 18%

Services

Management 9% ..............

Planning and

Management 15% .................................

..............

Property and Assets 6% .....................................

Asset Management 5%

Accounting 6% ..........................

Information Management 5% ..................

Procurement 4% ............

.........

Internal Controls 4% ..........

Cashier Operations 4% ...............

Special Accounts 2% ..................

57% Operations

13% Personnel

............................

........................................

.......................................

................................

6% Payroll Affairs

9% Lending

and Investment

37% Operations

...........................

...........................

........................................

...........................................

.......................................

.............................

Auditing

Auditing assists the Board of Directors and the

Board of Supervisors to examine the effectiveness of

internal controls, to measure and appraise the efficiency

and effectiveness of operations management, and to

identify actual or potential deficiencies. Audits also

provide timely suggestions for improvement, and follow-

up measures are implemented accordingly so as to

safeguard the effectiveness of fund management and to

ensure that operations are conducted transparently and

systematically.

Key Auditing Operations

Key auditing operations at the TaiwanICDF include:

(1) Examining the accuracy of financial and operational

information, and the security of the management of

capital, data and various securities; (2) examining internal

operations and determining whether procedures have

followed relevant policies, regulations and procedural

guidelines; (3) examining whether assets at the

TaiwanICDF, overseas missions and those allocated to

projects are being utilized effectively and are correctly

itemized; (4) examining whether completed operations

and projects met their intended objectives and achieved

the results anticipated; (5) investigating projects and

making onsite visits to overseas missions to examine the

status of internal controls, as well as the performance of

projects under implementation; (6) appraising operations

relating to the TaiwanICDF’s key reforms over recent

years and examining the progress and performance

of the organization’s annual work plan to ensure that its

objectives are realized efficiently and effectively; and (7)

reviewing the internal control systems by which each unit

performs its own supervision and monitoring to ensure the

integrity and results of associated reports compiled for the

Board of Directors.

Audits in 2014

A total of 33 audits were conducted in 2014, all

approved by either the Board of Directors or Board of

Supervisors. The content of these audits, representing

issues of concern to senior management and external

auditing units, focused on risks and internal controls.

Audits for 2014 were as follows: 12 related to

operations; six to accounting and cashier operations; five

to planning and management; three each to lending and

investment, and services management; and two each to

property and assets, and payroll affairs.

Results of Audits

In 2014, audits yielded a total of 115 suggestions: 66

on operations; 15 on personnel; seven on accounting;

six each on information management, and asset

management; five on procurement; four each on internal

controls, and cashier operations; and two on special

accounts.

Audits and subsequent conclusions were aimed

at strengthening internal controls and communication

between depa tments, raising colleagues’ awareness of

risks, guaranteeing the safety of the organization’s assets

and ensuring the reliability and accuracy of financial and

operational information.