81

promulgated by the Executive Yuan, and ROC Statement of Financial Accounting Standards No. 22 (“Accounting for

Income Taxes”). Under- or over-provision of income tax in the previous year is accounted for as an adjustment of

income tax expense in the current year.

15) Reserve for Contingencies of Guarantee Loss

The TaiwanICDF issues guarantees for private enterprises to secure loans in compliance with the Regulation for the

TaiwanICDF in Providing Guarantee for Credit Facilities Extended to Private Enterprises Which Invest in Countries with

Formal Diplomatic Relationships promulgated by MOFA. The reserve is accrued in accordance with the Regulation for

the TaiwanICDF Dealings with Past-Due/Non-Performing Loans and Bad Debts.

16) Revenues and Expenses

Revenues (including government donations) are recognized when the earning process is substantially completed and

is realized or realizable. Costs and expenses are recognized as incurred.

17) Use of Estimates

The preparation of financial statements in conformity with generally accepted accounting principles requires

management to make estimates and assumptions that affect the amounts of assets and liabilities and the disclosures

of contingent assets and liabilities at the date of the financial statements and the amounts of revenues and expenses

during the reporting period. Actual results could differ from those assumptions and estimates.

18) Settlement Date Accounting

The TaiwanICDF adopted settlement date accounting for the financial assets. For financial asset or financial liability

classified as at fair value through profit or loss, the change in fair value is recognized in profit or loss.

3. CHANGES IN ACCOUNTING PRINCIPLES

Receivables

On January 1, 2011, the TaiwanICDF adopted the renewed Financial Accounting Reporting Standard No. 34 of R.O.C.,

“Financial Instruments: Recognition and Measurement”. If the impairment would be approved by objective evidence, the

receivables and claim would be recognized as impairment loss. This change in accounting principle will not affect our

financial report of 2011.

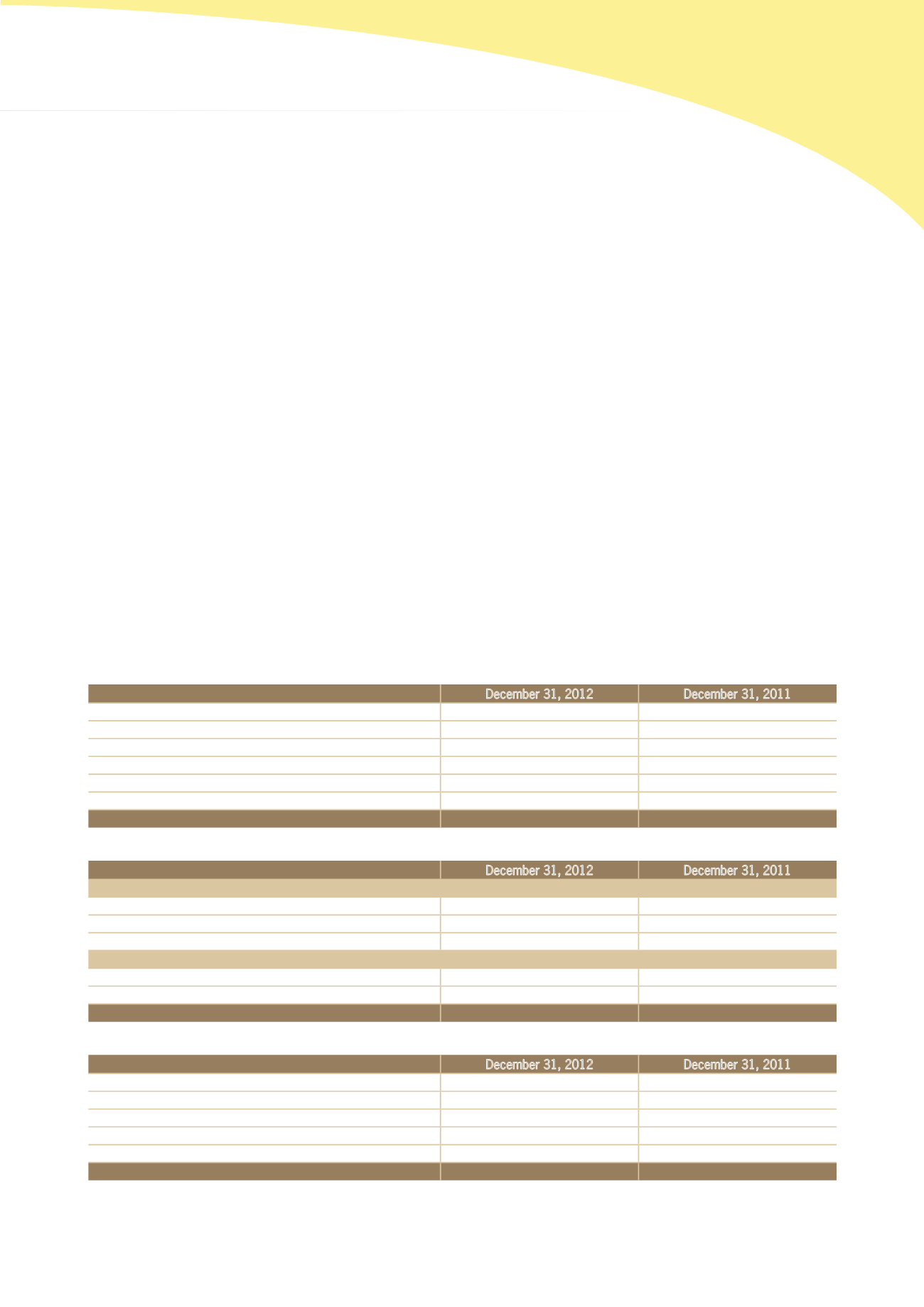

4. CASH AND CASH EQUIVALENTS

December 31, 2012

December 31, 2011

Petty cash

$110,000

$110,000

Demand deposits

287,487,458

158,915,101

Checking deposits

302,909

1,543,465

Time deposits

6,883,049,824

6,573,925,236

Cash equivalents

- Bonds purchased under resale agreements

50,000,000

180,000,000

Total

$7,220,950,191

$6,914,493,802

5. HELD-TO-MATURITY FINANCIAL ASSETS

December 31, 2012

December 31, 2011

Current items

Corporate bonds

$686,960,370

$200,034,151

Government bonds

–

206,921,232

$686,960,370

$406,955,383

Non-current items

Corporate bonds

$1,602,639,324

$2,086,354,374

Government bonds

–

–

$

1,602,639,324

$2,086,354,374

6. OTHER RECEIVABLES

December 31, 2012

December 31, 2011

Interest receivable

$105,678,884

$96,004,023

Retained money receivable on completed projects

43,289,622

29,809,443

Other recievables

15,556,316

16,854,724

Total

164,524,822

142,668,190

Less: Allowance for doubtful accounts

(812,117)

(930,568)

Net

$163,712,705

$141,737,622